Trying to navigate the ESG reporting can feel like learning a new language. Between CSRD, TCFD, IFRS, and more, sustainability consultants and ESG leads are faced with a growing list of overlapping acronyms, technical expectations, and evolving requirements.

Before diving into a deeper look, it’s helpful to clarify the difference between frameworks, standards and regulations:

- Frameworks (e.g., TCFD) provide guiding principles and disclosure recommendations. They outline what to consider but leave room for interpretation.

- Standards (e.g., ESRS E1 and IFRS S1/S2) are structured, enforceable rules that specify exactly what and how to report. They are typically adopted into law or regulatory mandates.

- Regulations (e.g., CSRD): are legally binding rules that mandate compliance, often incorporating standards and setting clear scope and deadlines.

This guide breaks down the core differences and overlaps between these frameworks and standards, focusing on physical climate risk reporting and ESG disclosure.

We’ll look at:

- ESRS E1 vs TCFD: How Europe’s climate standard relates to a global framework

- CSRD: How Europe sets corporate ESG disclosure requirements

- ESRS E1 vs IFRS S2: A comparison between two climate disclosure standards with different scopes and materiality lenses

You'll also see how Disclose supports alignment with different standards, helping consultants and internal teams generate consistent, asset-level physical climate risk disclosures across regions.

Quick summary: What each regulation, framework or standard entails

CSRD (Corporate Sustainability Reporting Directive)

A mandatory EU regulation that applies to over 50,000 companies. It requires detailed disclosures across environmental, social and governance (ESG) topics, underpinned by reporting standards (the ESRS, including ESRS E1 for physical climate risk).

CSRD introduces double materiality, meaning companies must report both on how sustainability issues affect them financially and how they impact people and the environment.

TCFD (Task Force on Climate-related Financial Disclosures)

A voluntary global framework that helped define best practices for climate-related financial disclosures. It focused on four pillars: governance, strategy, risk management, and metrics & targets.

Though the TCFD has officially been disbanded (as of 2023), its principles have been fully incorporated into IFRS S2 and remain foundational across climate standards globally.

IFRS S2 (International Sustainability Standards Board)

A global climate disclosure standard issued by the ISSB. IFRS S2 builds directly on TCFD and provides a detailed, scenario-based structure for disclosing physical and transition risks, climate-related governance, and financial impacts.

It prioritises financial materiality and is being adopted or referenced by jurisdictions including the UK, Australia, and California’s SB 261.

Comparison table: CSRD vs TCFD vs IFRS S2

What about other ESG frameworks and regulations?

CSRD, IFRS S2 and the legacy of TCFD are among the most relevant regulations, standards and frameworks for climate-related disclosures today.

But they sit within a much broader ESG reporting landscape that includes other regulations, taxonomies, and voluntary frameworks. For example:

- EU Taxonomy: is the European Union’s classification system that defines which economic activities can be considered environmentally sustainable. Companies subject to the CSRD must disclose Taxonomy-aligned data, which then serves as the foundation for assessing the share of sustainable revenues, CapEx, and OpEx.

- GRI (Global Reporting Initiative): is a voluntary sustainability reporting system focused on impact materiality, the effects an organization has on the environment and society. The GRI Standards are among the most widely used ESG standards worldwide and are designed to support broad stakeholder reporting. They are interoperable with the CSRD, helping companies streamline disclosures and avoid duplication when reporting under both the voluntary GRI Standards and the mandatory CSRD requirements.

- CSDDD (Corporate Sustainability Due Diligence Directive): is an upcoming EU regulation that will require companies to identify, prevent, and mitigate human rights and environmental risks across their value chains. While CSDDD is about due diligence processes and accountability, the CSRD provides the complementary disclosure layer, requiring companies to report on risks, impacts, and due diligence measures in line with the ESRS.

- SFDR (Sustainable Finance Disclosure Regulation): A mandatory EU regulation targeting financial market participants (e.g. asset managers). SFDR requires transparency on how sustainability risks, impacts, and objectives are integrated into investment processes. SFDR product-level disclosures rely heavily on company-level ESG data, primarily sourced from CSRD reports.

Disclose was built to support climate-related disclosures under CSRD (via ESRS E1), IFRS S2 and TCFD (via IFRS S2).

This makes it a valuable input to broader ESG and sustainability workflows, including those involving investor reporting, supply chain risk, and financial materiality assessments.

How ESG consultants use Disclose across reporting standards

Let’s say you're advising a renewable energy company with operations in both Europe and California. They need to report under CSRD in the EU and SB 261 in the US, which recommends alignment with a recognised climate disclosure standard such as IFRS S2. But they want to avoid running separate physical climate risk assessments for each region.

With Disclose, you can run a single, science-backed analysis and generate outputs aligned with both ESRS E1 (the climate standard under CSRD) and IFRS S2 without needing additional modelling teams or involving 3rd parties.

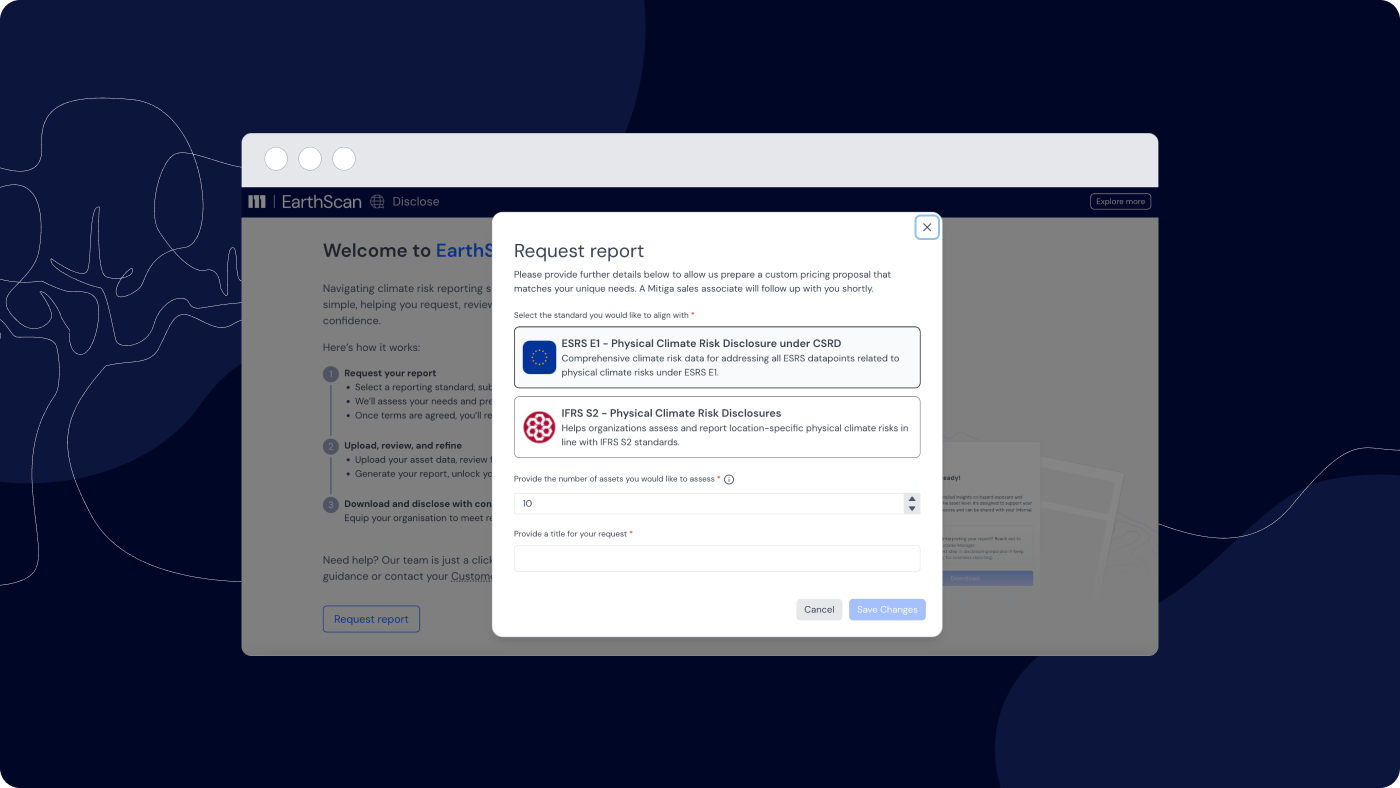

How it works

- Upload a CSV of asset locations

- Select your reporting standard: ESRS E1 or IFRS S2

- Receive fully quantified physical climate risk outputs, including: Per-hazard risk scores, financial exposure estimates (e.g. CVaR for flood and extreme wind), and disclosure-ready narrative aligned to each standard

Disclose quantifies physical climate risks like flood, wildfire, and extreme heat, modelled using Mitiga’s proprietary EarthScan hazard engine.

This engine combines asset-level data with high-resolution Earth system models, delivering results across three timeframes (2025, 2030, 2060) and three climate scenarios (business-as-usual, Paris-aligned, and delayed transition).

No in-house modelling expertise required. Our reporting solution includes modelling for you.

For ESG consultants, this means:

- One tool to support CSRD (via ESRS E1), IFRS S2, and regulations requiring IFRS-aligned disclosures, such as SB 261

- Accelerated, cost-efficient analysis that saves hours of manual work

- Audit- and investor-ready reports that meet growing stakeholder expectations

Disclose becomes your single source of truth for physical climate risk, whether your clients are reporting under CSRD (ESRS E1), aligning with SB 261, or preparing for future regulatory or investor-led reviews.

Conclusion: One tool, no duplicated effort

Navigating CSRD, IFRS S2, and other ESG reporting requirements is a core challenge for sustainability teams and consultants. Corporations expect clarity, speed, and consistency, even across different regulatory regimes.

And with growing overlap between standards, expectations from regulators, investors, and auditors are only increasing.

Disclose cuts through the complexity. From a simple CSV of asset locations, it generates science-backed physical climate risk reports aligned with ESRS E1 and IFRS S2.

Whether you're supporting Article 9 funds, wave-one CSRD reporters, or California-based companies preparing for SB 261 or other local regulations, Disclose gives you:

- Consistent outputs aligned to multiple standards

- Automated climate risk modelling

- Narrative text and financial estimates ready for disclosure

Want to see it in action? Book a demo today and see how Disclose can streamline your next physical climate disclosure.