As climate-related risks intensify and regulatory expectations evolve, companies face growing pressure to demonstrate that they understand and manage their exposure to physical climate hazards.

Yet a persistent misconception remains: that credible climate risk disclosure requires assessing all possible hazards, regardless of their relevance to the business.

Our latest research, Hazards coverage: A data-driven look at material climate hazards in sustainability reports challenges that notion.

Drawing on disclosures from 100 global leaders across 10 industries, the report reveals how organisations are approaching hazard screening in practice, what they’re choosing to disclose, and how these decisions align with frameworks like CSRD, TCFD, and ISSB.

This article explores the findings in depth, clarifies what physical climate hazards are, and explains how regulatory standards define materiality. It also examines why most companies disclose only a fraction of the hazards listed in the EU Taxonomy, and how a focused, defensible approach to screening can strengthen both compliance and credibility.

To begin, let’s take a closer look at what physical climate hazards actually are and why they matter in the context of climate risk reporting.

What are physical climate hazards?

Physical climate hazards are acute or chronic events and trends, such as floods, wildfires, droughts, and extreme temperatures, that can disrupt operations, damage assets, and impact financial performance.

These hazards are increasingly central to climate risk assessments and disclosures.

To support companies in identifying relevant risks, the European Commission published a reference list of 28 physical climate hazards in the EU Taxonomy.

This list, also referenced in ESRS E1, includes:

- Flood (coastal, fluvial, pluvial, groundwater)

- Wildfire

- Drought

- Changing temperature

- Solifluction

- Avalanche

- Glacial lake outburst

- ...and many more

While comprehensive, the EU hazard table is indicative, not prescriptive. It is intended to serve as a baseline for climate risk and vulnerability assessments, not a checklist for mandatory disclosure.

What ESRS E1 and IFRS S2 actually require

Both ESRS E1 and IFRS S2 require companies to disclose physical climate risks, but neither mandates disclosure of all 28 hazards.

- ESRS E1 expects companies to screen the full EU hazard table but only disclose those hazards that are material to their operations, value chain, or stakeholders. It applies a double materiality lens, considering both financial and impact materiality.

- IFRS S2 does not reference the EU table. Instead, it requires disclosure of material climate-related risks, categorised as acute or chronic, based on a company’s own risk assessment. It applies a financial materiality lens only.

In both cases, the emphasis is on defensibility, not exhaustiveness. Companies must be able to justify which hazards they disclose and which they exclude, based on a transparent, evidence-based screening process.

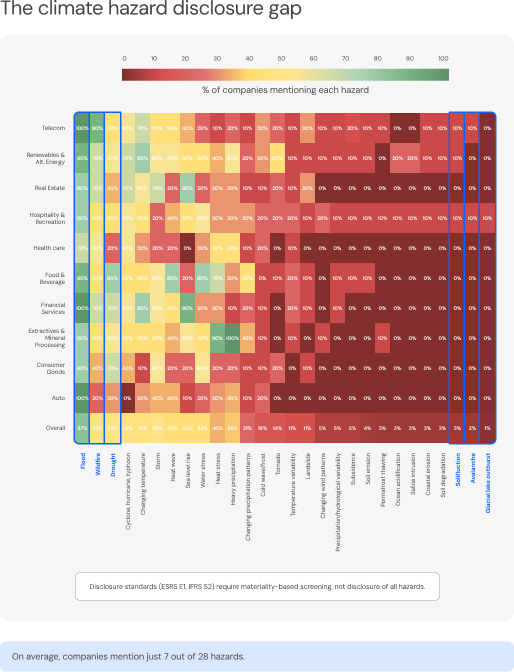

Key findings from our hazard coverage report

To understand how companies are currently approaching hazard disclosure, Mitiga Solutions analysed sustainability reports from 100 global leaders across 10 key industries.

The results reveal a striking pattern:

- On average, companies assess just 7 out of 28 physical climate hazards, roughly 25% of the EU Taxonomy list.

- The most commonly disclosed hazards are:

- Flood: referenced by 87% of companies

- Wildfire: 57%

- Drought: 53%

- The least disclosed hazards include:

- Solifluction: 3%

- Avalanche: 2%

- Glacial lake outburst: 1%

This suggests that even among industry leaders, companies are selective in their hazard assessments, focusing on those most relevant to their business context.

📥 Download the full report to explore sector-by-sector benchmarks and hazard coverage patterns.

Why materiality-based screening is the right approach

The findings reinforce a critical point: materiality, not completeness, is the foundation of credible climate risk disclosure.

- Screening is mandatory under ESRS E1, but disclosure is selective.

- Companies must assess the likelihood and severity of each hazard’s impact on their operations, assets, and supply chains.

- A defensible, data-driven screening process is essential to meet auditor and regulator expectations.

This approach not only aligns with regulatory requirements, it also ensures that disclosures are decision-useful, focused on the risks that truly matter.

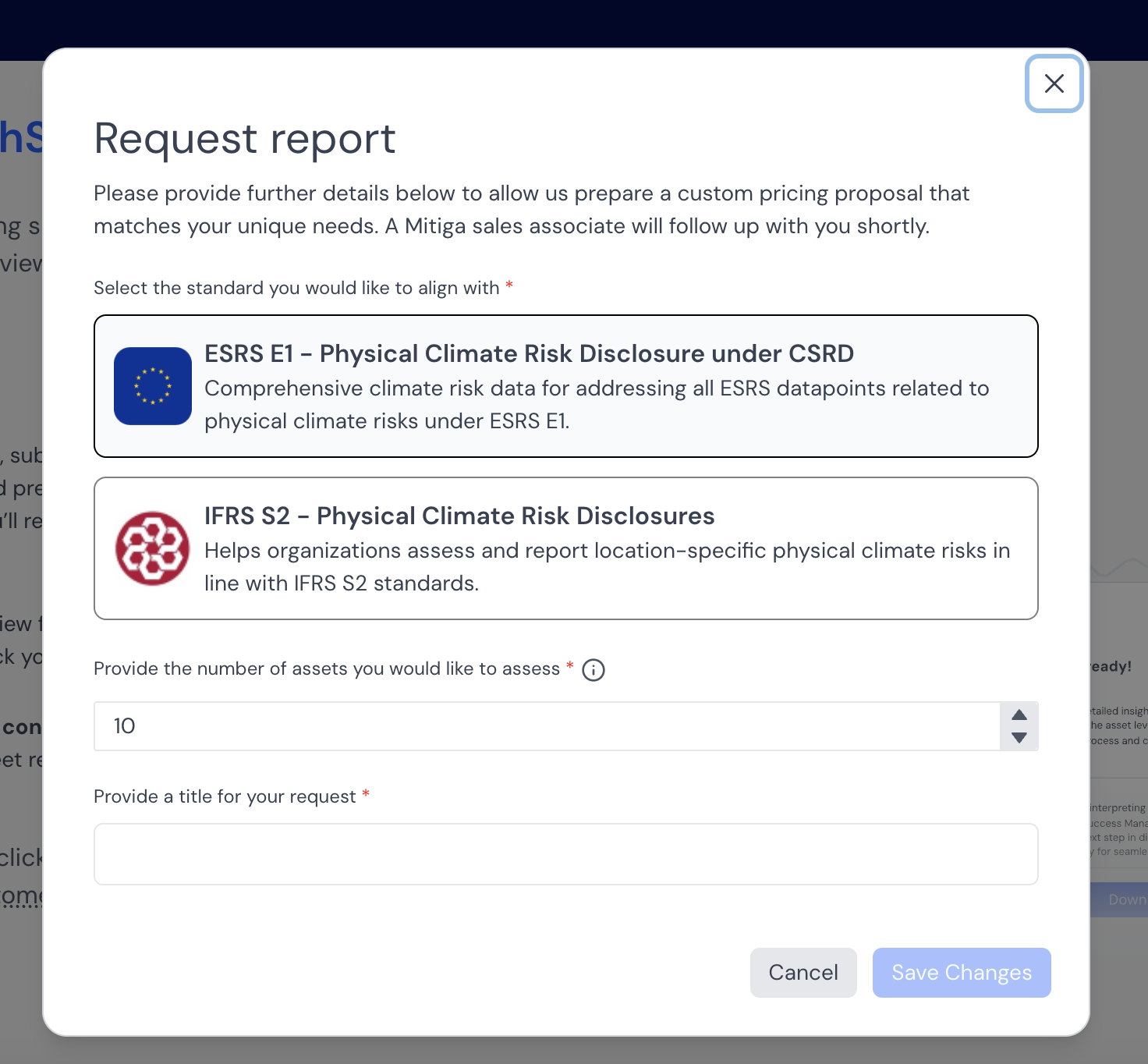

How Mitiga Solutions' Disclose simplifies hazard screening

For many organisations, the challenge isn’t recognising the importance of hazard screening, it’s doing it efficiently, defensibly, and at scale.

That’s where our Disclose tool comes in.

Disclose is Mitiga Solutions’ fully automated physical climate risk disclosure tool. Built for sustainability teams, ESG consultants, and investors, it helps organisations:

- Screen for the most material hazards, starting with those most commonly reported, like flood, wildfire, and changing temperature

- Generate standard-aligned outputs, both narrative and quantitative, mapped to regulatory fields

- Reduce manual effort and cost, with no internal modelling expertise or third-party consultants required

- Scale with confidence, from 5 to 5,000 assets, across three climate scenarios and time horizons

- Accelerate compliance with ESRS E1 (CSRD), IFRS S2, and TCFD

- Strengthen audit defensibility with science-backed insights

- Deliver faster, higher-quality disclosures without the overhead

Disclose transforms climate risk reporting from a regulatory burden into a strategic advantage.

👉 Learn more about Disclose

Conclusion: Focus on what matters

Our research confirms what many sustainability and risk professionals already suspect: most companies are not disclosing all 28 physical climate hazards and they don’t need to.

What they do need is a defensible, efficient, and standard-aligned way to screen for material risks and report them with confidence.

Whether you're a first-time reporter or a seasoned sustainability lead, our benchmarking report offers a valuable reference point. It helps you understand how your peers are approaching hazard disclosure and how you can do the same, better.